As 2025 comes to a close, the U.S. RV industry is not facing a demand collapse. It’s facing a pricing and inventory discipline problem.

For RV dealers across the United States, this year delivered a clear message:

Inventory still sells, but only when pricing, timing, and market velocity are aligned.

With 2026 and early 2027 RV models entering dealer pipelines, the lessons from 2025 are now shaping how smart dealerships must approach RV pricing strategy, inventory aging, and cash flow management going forward.

Data Note

Insights in this article are based on Rapidious Titan.AI analysis of RV listings and sales transactions across the U.S. over the last 12 months, spanning new and used inventory across all major RV categories. Rapidious Titan.AI aggregates real transaction data from across the U.S. RV market to give dealers live pricing intelligence, inventory velocity benchmarks, and aging risk signals.

What Really Happened in the U.S. RV Market in 2025

From the outside, 2025 felt slow.

From the data, it was uneven and unforgiving.

According to Rapidious Titan.AI analysis of nationwide RV listing and sales trends:

- New RVs averaged 195 days to sell

- Used RVs sold faster, averaging 117 days on lot

- Nearly 50% of all RV inventory sat beyond 90 days

- More than $6.48 billion in RV inventory remained tied up on dealer lots

- At roughly 1% monthly carrying cost, this created $778+ million in annual floorplan losses for U.S. dealers

This was not caused by disappearing RV buyers.

It was caused by inventory aging faster than pricing strategies adjusted.

Pricing Became the Real Demand Filter

One of the clearest lessons from the 2025 RV market is that buyers are still active, but far less forgiving.

Rapidious Titan.AI market data shows:

- 19% of RV inventory sold within the first 30 days

- Another 32% sold between 31–90 days

- Over 50% of RVs moved at a healthy pace, when priced correctly

Once a unit missed the market early:

- Shopper perception shifted

- Lead volume dropped

- Discounts became reactive instead of strategic

- Margin erosion accelerated

2026 Takeaway for RV Dealers:

Pricing can no longer be set once and revisited later.

In 2026, RV pricing must evolve dynamically based on:

- Days on lot

- Competitive listings

- Regional demand

- Model-year exposure

What Dynamic Pricing Means in Practice

Dynamic pricing does not mean constant discounting or giving up control. It means reviewing inventory performance on a defined cadence (weekly or bi-weekly), monitoring comparable listings within your competitive radius, and triggering structured price evaluations at key aging points such as 30, 60, and 75 days on lot.

Dealers always retain full control over the final price. Data and technology can recommend adjustments based on market conditions, but changes should move through an internal approval mechanism. The goal is not automatic discounting, it is faster, data-informed decision-making before inventory becomes stale.

The 90-Day Rule Defined RV Dealer Profitability in 2025

If 2025 established one hard rule for U.S. RV dealerships, it was this:

Once an RV crosses 90 days on lot, it becomes a financial liability.

After Day 90:

- Floorplan interest compounds

- Depreciation accelerates

- Gross margins collapse

According to Rapidious Titan.AI analysis, in 2025 alone RV inventory aged beyond 90 days cost U.S. dealers nearly $65 million per month in carrying expenses.

2026 Strategy Shift

Top-performing RV dealers now treat Day 90 as an action trigger, not a waiting point.

Pricing adjustments must happen before inventory becomes stale, not after.

Why Used RV Inventory Outperformed New RVs

Used RVs sold 67% faster than new units in 2025, highlighting a major shift in buyer behavior.

This doesn’t mean new RV demand disappeared.

It means buyers became far more value-driven and price-aware.

What This Means for 2026:

- Used RV inventory will remain a velocity anchor

- New RVs must be stocked intentionally

- Overbuying new units without a clear turnover plan increases risk

- Model-year aging is now a real pricing penalty

New RVs will sell in 2026, but only when pricing accuracy and inventory discipline are in place from Day 1.

The 2025 Model Year Became the Industry’s Pressure Point

By late 2025, Rapidious Titan.AI data showed over $3.77 billion in 2025 RV models remained unsold, with average age exceeding 7 months as 2026 models drew buyer attention and 2027 production loomed.

As model years stacked up, "new but aged" inventory lost value daily.

Dealers felt pressure from buyers demanding discounts, lenders tightening floorplan terms, and OEM incentives undercutting older units.

Lesson RV dealers must take for 2026: model-year exposure must be managed proactively. Waiting turns depreciation into a forced loss.

Geography Played a Bigger Role Than Expected

Where RV inventory sat mattered just as much as what it was.

- Florida maintained strong RV sales velocity despite high inventory levels, supported by year-round demand and seasonal population flow.

- Texas, Utah, and Colorado absorbed inventory faster than national averages, likely driven by strong outdoor recreation demand and pricing alignment with local competition.

- States like South Dakota, Maryland, and North Dakota showed extended aging and weaker demand, reflecting tighter regional buyer pools and slower pricing adjustments.

Dealers who:

- Monitor regional RV demand

- Adjust pricing by market

- Transfer inventory across states

- Align stocking with proven demand corridors

…can dramatically improve turn rates and cash flow.

RV Market Forecast 2026: What U.S. RV Dealers Should Prepare For

The RV market entering 2026 will not reward patience, it will reward speed and discipline.

Dealers who succeed will:

- Adjust pricing early

- Enforce strict aging policies

- Balance new and used RV inventory

- Align stocking with real market velocity

- Act before inventory becomes a problem

Those who wait for seasonal demand or delay hard decisions will continue absorbing unnecessary floorplan costs.

Final Outlook for U.S. RV Dealers

2025 was a warning.

2026 will test execution.

For U.S. RV dealerships, success next year will not be defined by lot size, OEM allocations, or brand mix alone. It will be defined by inventory turn speed, pricing accuracy, aging control, and market awareness.

In 2026, the RV dealers who act early will lead the market.

2026 Action Checklist for RV Dealers

As you plan for 2026, these are the questions every RV dealer should be able to answer with data - not gut feel:

- Are we reviewing pricing on a consistent weekly cadence?

- Do we have structured aging triggers at 30, 60, and 75 days?

- Are we managing model-year exposure before new inventory arrives?

- Is our new vs. used mix aligned with real market velocity?

- Are we pricing based on local competition rather than broad averages?

- Can pricing adjustments move through our approval process quickly?

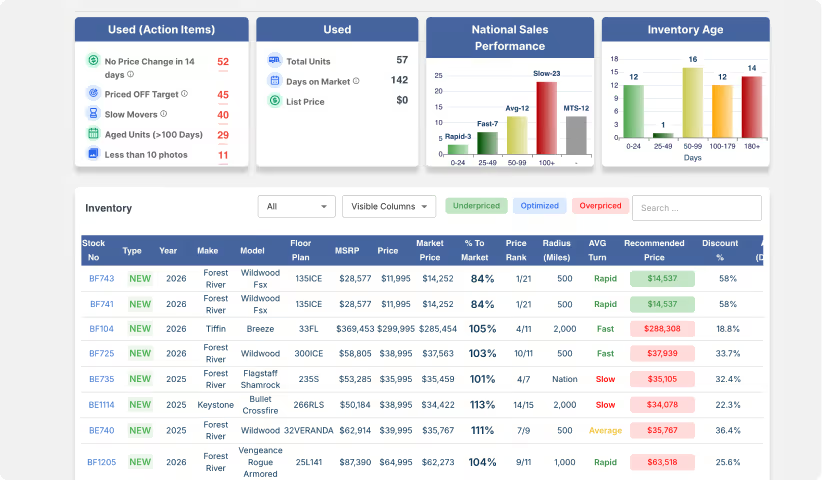

Dealers using Rapidious Titan.AI can answer every one of these questions from a single dashboard - with live transaction data, VIN-level aging signals, regional competitive pricing, and model-year velocity benchmarks updated continuously. The goal is not to replace dealer judgment on these decisions, but to make sure that judgment is backed by what the market is actually doing, not what it did six months ago.

How Rapidious Titan.AI Supports 2026 Execution

The market intelligence described throughout this forecast is not theoretical. It is what Rapidious Titan.AI surfaces for RV dealers every day.

In practice, that means:

- Live price-to-market benchmarking across local, regional, and national competing rooftops - so pricing decisions reflect what the market is clearing at today, not last month

- VIN-level aging and turn data that flags units trending behind their national velocity benchmark - before they cross the thresholds where margin recovery becomes difficult

- Model-year exposure visibility across new and used inventory - so dealers can act on carryover risk before it compounds into a floorplan problem

- Regional demand signals by geography - so stocking and transfer decisions are grounded in where inventory is actually moving, not national averages

- Real transaction data on what comparable units actually sold for and how fast - not asking prices from listing sites

2025 exposed the cost of pricing without complete market visibility. Rapidious Titan.AI is built so that 2026 does not have to repeat it.

.svg)

-

Heading 2

Heading 3

Heading 4

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do

Ordered list

Unordered list

Text link

Bold text

Emphasis

-