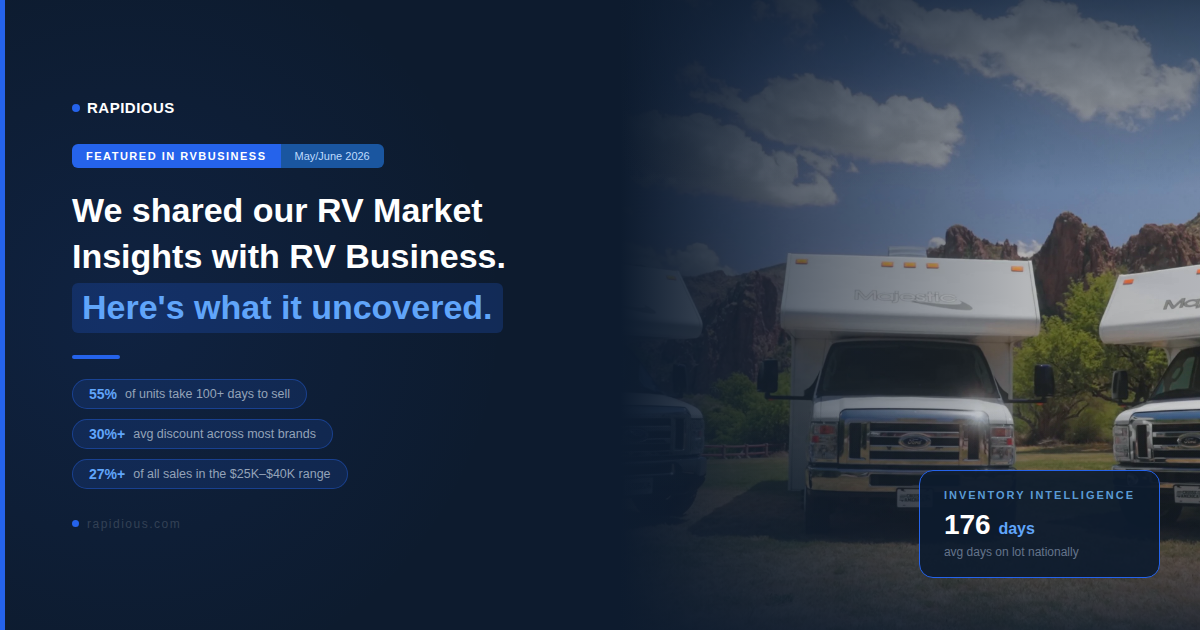

A Fresh Data-Driven Look at 130,607 U.S. RV Listings

A new Rapidious Titan.AI analysis of 130,607 active RV listings across the U.S. shows that widely accepted truths about pricing, stocking, and turnover are no longer aligned with real-world data.

The biggest takeaway? Dealers aren't just dealing with aging inventory - they're misreading demand altogether. And when demand is misread, floorplan costs rise, ordering becomes reactive, and profit potential shrinks.

Myth #1: “Entry-Level RVs Sell the Fastest.”

Reality: Luxury RVs ($100k+) Turn Faster Than Budget Units.

According to Rapidious Titan.AI analysis of 130,607 U.S. listings:

- Budget RVs (<$30k): 164 days average age

- Luxury RVs ($100k+): 153 days average age

- Fresh inventory under 50 days old: Budget units 23.5% vs Luxury units 31.0%

Luxury buyers, despite a smaller segment, are decisive, consistent, and less price-sensitive - leading to faster turns and higher-margin opportunities.

Myth #2: “Lower Prices Always Improve Turns.”

Reality: The Midwest Has the Slowest Turnover, Even With Lower Prices.

Rapidious Titan.AI inventory data shows:

- Midwest average age: 168.8 days

- West Coast average age: 144.8 days

- Midwest average price: $55,986

- West Coast average price: $61,403

Despite lower prices, Midwest inventory ages 24 days longer on average. This isn't a pricing issue - it's a market saturation issue. The Midwest holds 25.7% of national inventory, creating oversupply that suppresses turnover regardless of price.

Myth #3: “Popular Models Are Always Safe to Stock Deep.”

Reality: Coleman Trims Are Oversaturated, and Dealers Don’t Realize It.

According to Rapidious Titan.AI market data, Keystone's Coleman line represents 4.75% of the entire U.S. RV market. Three trims alone (13B, 17B, 17R) represent 2,603 units nationally.

The 17R trim is the warning sign: 228 days average age - 7.6 months on lots. This is no longer a high-volume favorite. It is a market saturation risk.

Dealers holding more than 15% Coleman inventory are exposed to declines in entry-level demand that haven't been fully realized yet - a risk that could compress margins across multiple states.

Myth #4: “Premium Brands Perform the Same Regardless of State.”

Reality: Geography Determines Premium RV Success.

Rapidious Titan.AI data shows premium brand performance varies dramatically by state:

- California: 137-day average age, strongest luxury demand, fresh premium inventory

- Oklahoma: 321-day average age - units aging 2.3x longer than California

Manufacturers continue shipping high-end units into markets that cannot absorb them, resulting in artificial discounting, brand erosion, unnecessary floorplan costs, and dealers stuck with 6-12 months of premium inventory.

Myth #5: “Holding Out for Retail Pricing Always Pays Off.”

Reality: Nearly 10% of RV Inventory Has Been Sitting for Over a Year.

According to Rapidious Titan.AI analysis, 12,823 units nationwide have crossed the 365+ day threshold, now averaging 503 days - that is 1.38 years of accumulating costs.

This segment alone represents $784 million in trapped inventory value, based on Rapidious Titan.AI data.

Top contributors: Forest River (3,578 units over a year old), Keystone (1,369 units), Jayco (942 units).

With floorplan rates at 8%, Rapidious Titan.AI estimates dealers are absorbing $63.5M per year in interest on this aging segment alone. These units no longer have retail pricing potential - they require decisive liquidation strategies.

What This Means for Dealers: The Real Problem Is Misreading Demand

These myths reveal a painful truth:

Dealers are not operating with real-time demand signals.

The industry still relies on assumptions from 2018–2020, but the market of 2025 behaves very differently. Oversupply in some regions, misallocated premium brands, saturated entry-level segments, and underappreciated luxury momentum all point to one conclusion:

Dealers who rely on intuition will fall behind those who rely on data.

How Rapidious Titan.AI Surfaces the Data Behind These Myths

The five myths in this analysis persist because most dealers don't have a live, granular view of what the market is actually doing - by model, by region, by price segment. Rapidious Titan.AI is built on exactly that data.

In practice, that means:

- Velocity benchmarks by model and price segment - so dealers see whether luxury or budget units are actually turning faster in their specific market, not just nationally

- Regional supply saturation signals - so stocking decisions reflect local inventory concentration, not manufacturer allocation patterns

- VIN-level aging data that shows which units are approaching the thresholds where liquidation becomes the better financial decision than continued carrying costs

The dealers who stop misreading demand are the ones who replace assumptions with live market data. Rapidious Titan.AI provides that data layer across all 50 U.S. states.

.svg)

-

Heading 2

Heading 3

Heading 4

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do

Ordered list

Unordered list

Text link

Bold text

Emphasis

-